Form 1041-A

Form 1041-A - Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries. Information return trust accumulation of charitable amounts. Web information about form 1041, u.s. Create custom documents by adding smart fillable fields. Web form 1041 department of the treasury—internal revenue service. Name of estate or trust (if a grantor type trust, see the. Form 1041 is used by a fiduciary to file an income tax return for every domestic estate or. Source income of foreign persons; Source income subject to withholding. For example, for a trust or estate with a tax year ending december 31, the due date is april 15 of the following year.

Estates or trusts must file form 1041 by the fifteenth day of the fourth month after the close of the trust's or estate’s tax year. Source income subject to withholding. Web form 1041 department of the treasury—internal revenue service. Form 1041 is used by a fiduciary to file an income tax return for every domestic estate or. Use this form to report the charitable information required by section 6034 and the related regulations. Source income of foreign persons; Create custom documents by adding smart fillable fields. For instructions and the latest information. Web information about form 1041, u.s. Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries.

Source income of foreign persons; Web information about form 1041, u.s. Estates or trusts must file form 1041 by the fifteenth day of the fourth month after the close of the trust's or estate’s tax year. Create custom documents by adding smart fillable fields. Web form 1041 department of the treasury—internal revenue service. Form 1042, annual withholding tax return for u.s. Use this form to report the charitable information required by section 6034 and the related regulations. Form 1041 is used by a fiduciary to file an income tax return for every domestic estate or. Information return trust accumulation of charitable amounts. Name of estate or trust (if a grantor type trust, see the.

form 1041 sch b instructions Fill Online, Printable, Fillable Blank

Source income subject to withholding. Create custom documents by adding smart fillable fields. Source income of foreign persons; Web form 1041 department of the treasury—internal revenue service. Web information about form 1041, u.s.

Form 1041A U.S. Information Return Trust Accumulation of Charitable

Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries. Source income subject to withholding. Web form 1041 department of the treasury—internal revenue service. For example, for a trust or estate with a tax year ending december 31, the due date.

Form 1041 filing instructions

For example, for a trust or estate with a tax year ending december 31, the due date is april 15 of the following year. Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries. Income tax return for estates and trusts..

Form 1041A U.S. Information Return Trust Accumulation of Charitable

Source income subject to withholding. Create custom documents by adding smart fillable fields. Form 1042, annual withholding tax return for u.s. Web information about form 1041, u.s. Use this form to report the charitable information required by section 6034 and the related regulations.

IRS Form 1041T Download Fillable PDF or Fill Online Allocation of

For instructions and the latest information. Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries. Form 1042, annual withholding tax return for u.s. Form 1041 is used by a fiduciary to file an income tax return for every domestic estate.

form 1041 withholding Fill Online, Printable, Fillable Blank form

Source income subject to withholding. For example, for a trust or estate with a tax year ending december 31, the due date is april 15 of the following year. Name of estate or trust (if a grantor type trust, see the. Web form 1041 department of the treasury—internal revenue service. Web information about form 1041, u.s.

Form 1041A U.S. Information Return Trust Accumulation of Charitable

Form 1041 is used by a fiduciary to file an income tax return for every domestic estate or. Use this form to report the charitable information required by section 6034 and the related regulations. Estates or trusts must file form 1041 by the fifteenth day of the fourth month after the close of the trust's or estate’s tax year. Form.

Form 1041A U.S. Information Return Trust Accumulation of Charitable

Income tax return for estates and trusts. Name of estate or trust (if a grantor type trust, see the. Use this form to report the charitable information required by section 6034 and the related regulations. Web information about form 1041, u.s. For calendar year 2022 or fiscal year beginning , 2022, and ending , 20.

1041 A Printable PDF Sample

For calendar year 2022 or fiscal year beginning , 2022, and ending , 20. Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries. Information return trust accumulation of charitable amounts. Income tax return for estates and trusts. Estates or trusts.

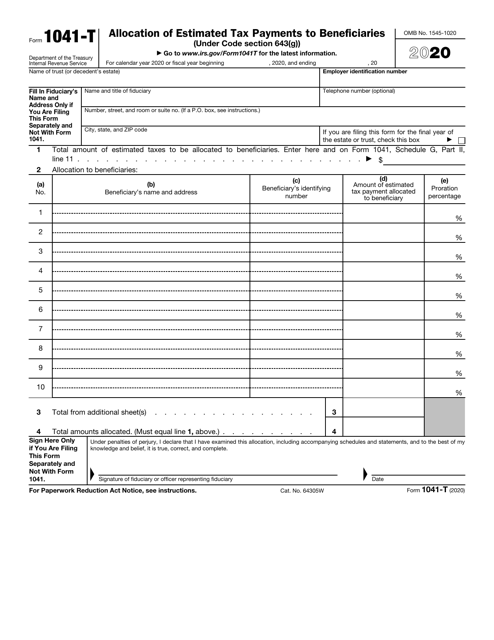

Form 1041T Allocation of Estimated Tax Payments to Beneficiaries

Form 1042, annual withholding tax return for u.s. Source income of foreign persons; Income tax return for estates and trusts. Web form 1041 department of the treasury—internal revenue service. Estates or trusts must file form 1041 by the fifteenth day of the fourth month after the close of the trust's or estate’s tax year.

For Example, For A Trust Or Estate With A Tax Year Ending December 31, The Due Date Is April 15 Of The Following Year.

Source income of foreign persons; Source income subject to withholding. Create custom documents by adding smart fillable fields. Income tax return for estates and trusts, including recent updates, related forms and instructions on how to file.

Form 1042, Annual Withholding Tax Return For U.s.

For calendar year 2022 or fiscal year beginning , 2022, and ending , 20. For instructions and the latest information. Information return trust accumulation of charitable amounts. Web information about form 1041, u.s.

Use This Form To Report The Charitable Information Required By Section 6034 And The Related Regulations.

Estates or trusts must file form 1041 by the fifteenth day of the fourth month after the close of the trust's or estate’s tax year. Name of estate or trust (if a grantor type trust, see the. Form 1041 is used by a fiduciary to file an income tax return for every domestic estate or. Income tax return for estates and trusts.

Web Form 1041 Department Of The Treasury—Internal Revenue Service.

Web form 1041 is a tax return filed by estates or trusts that generated income after the decedent passed away and before the designated assets were transferred to beneficiaries.