Form 966 Penalty

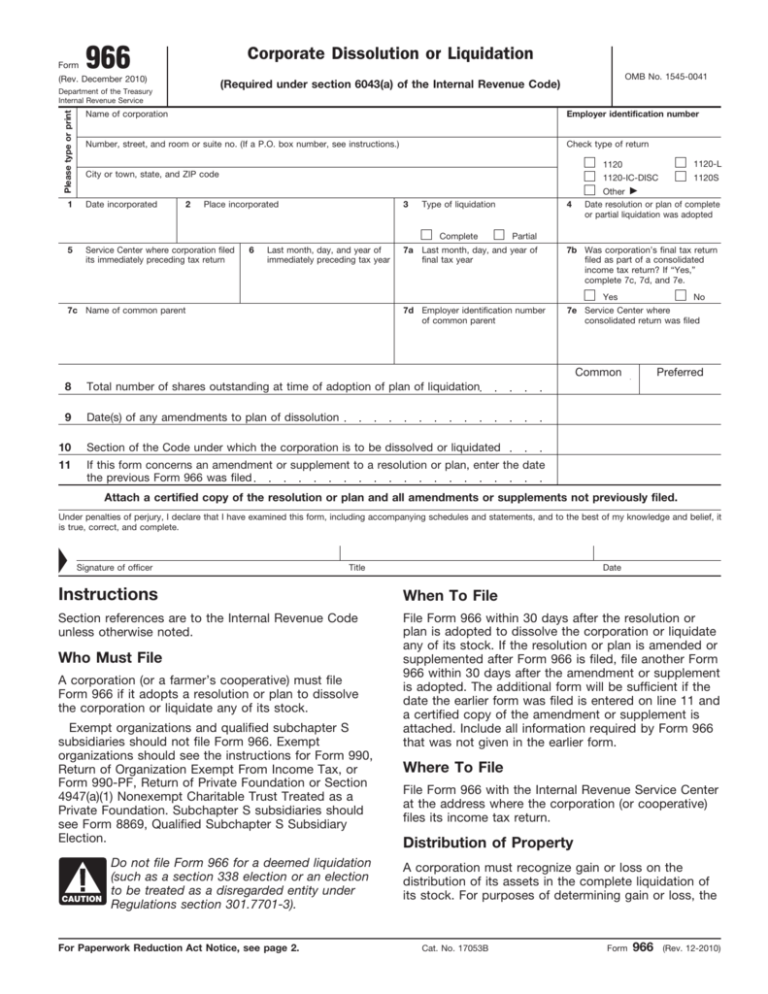

Form 966 Penalty - Distribution of property corporation must recognize gain or loss on the distribution of its assets in the complete liquidation of its stock. 6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or dissolution, there does not appear to be any specific penalty attached for failing to file it. Absent a penalty authorized in the law, there is literally no penalty for failing to file form 966. For purposes of determining gain or loss, the Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return. This is especially true when there are foreign corporations involved, which may lead to form 5471 penalties and an. A corporation (or a farmer’s cooperative) files this form if it adopts a resolution or plan to dissolve the corporation or liquidate any of its stock. That section, however, has no provision for penalties for violations of 6043(a). Web once a corporation adopts a plan of liquidation and files the proper state paperwork (if required), it must send form 966, corporate dissolution or liquidation, with a copy of the plan to the irs within 30 days after the date of the adoption. Web who must file form 966?

Absent a penalty authorized in the law, there is literally no penalty for failing to file form 966. Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return. Web who must file form 966? A corporation, or farmer’s cooperative, must file form 966 if it plans to dissolve the corporation or liquidate the company’s stock, in accordance with internal revenue code section 6043(a). 6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or dissolution, there does not appear to be any specific penalty attached for failing to file it. Get information on coronavirus relief for businesses. Distribution of property corporation must recognize gain or loss on the distribution of its assets in the complete liquidation of its stock. For purposes of determining gain or loss, the That section, however, has no provision for penalties for violations of 6043(a). This is especially true when there are foreign corporations involved, which may lead to form 5471 penalties and an.

This is especially true when there are foreign corporations involved, which may lead to form 5471 penalties and an. Web form 966 penalty vs indirect penalty. Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return. Absent a penalty authorized in the law, there is literally no penalty for failing to file form 966. Web the basic penalty for failing to file a form 966 within 30 days of adopting the resolution to dissolve is $10 per day. Get information on coronavirus relief for businesses. That section, however, has no provision for penalties for violations of 6043(a). However, there are some special rules, depending on the situation, type of business and the type of liquidation. Web who must file form 966? Web they must file form 966, corporate dissolution or liquidation, if they adopt a resolution or plan to dissolve the corporation or liquidate any of its stock.

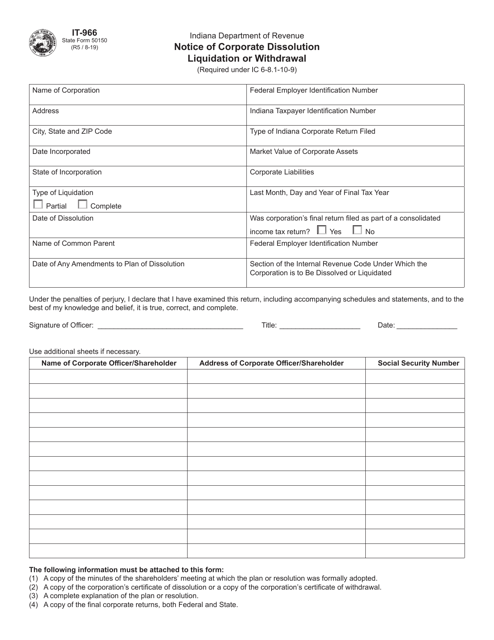

Form IT966 (State Form 50150) Download Fillable PDF or Fill Online

Web information about form 966, corporate dissolution or liquidation, including recent updates, related forms and instructions on how to file. Web who must file form 966? However, there are some special rules, depending on the situation, type of business and the type of liquidation. Web once a corporation adopts a plan of liquidation and files the proper state paperwork (if.

IRS Cover Letter for 966

For purposes of determining gain or loss, the A corporation (or a farmer’s cooperative) files this form if it adopts a resolution or plan to dissolve the corporation or liquidate any of its stock. Get information on coronavirus relief for businesses. 6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or.

Form 966 (Rev PDF Tax Return (United States) S Corporation

Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return. Closing your business can be a difficult and challenging task. For purposes of determining gain or loss, the This is especially true when there are foreign corporations involved, which may lead to form 5471.

AR2210 Individual Underpayment of Estimated Tax Penalty Form

Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return. Absent a penalty authorized in the law, there is literally no penalty for failing to file form 966. This is especially true when there are foreign corporations involved, which may lead to form 5471.

Penalty for Not Filing IRS Form 966 Bizfluent

Web the basic penalty for failing to file a form 966 within 30 days of adopting the resolution to dissolve is $10 per day. Get information on coronavirus relief for businesses. Distribution of property corporation must recognize gain or loss on the distribution of its assets in the complete liquidation of its stock. Web they must file form 966, corporate.

Penalty Waive off on Late GST Filling To TaxFin Online Taxt

For purposes of determining gain or loss, the However, the maximum penalty for the organization for failing to file any single form 966 is $5,000. Web penalties for failing to file documents required by section 6043 of the tax code are spelled out in section 6652. Web where to file file form 966 with the internal revenue service center at.

How to Complete IRS Form 966 Bizfluent

Web form 966 penalty vs indirect penalty. A corporation (or a farmer’s cooperative) files this form if it adopts a resolution or plan to dissolve the corporation or liquidate any of its stock. Closing your business can be a difficult and challenging task. Web penalties for failing to file documents required by section 6043 of the tax code are spelled.

Form 966 (Rev. December 2010)

Web the basic penalty for failing to file a form 966 within 30 days of adopting the resolution to dissolve is $10 per day. 6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or dissolution, there does not appear to be any specific penalty attached for failing to file it. A.

Form 89224 Download Fillable PDF or Fill Online Request for Waiver of

Closing your business can be a difficult and challenging task. 6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or dissolution, there does not appear to be any specific penalty attached for failing to file it. Web once a corporation adopts a plan of liquidation and files the proper state paperwork.

정액환급율표고시 신청서 샘플, 양식 다운로드

Web the basic penalty for failing to file a form 966 within 30 days of adopting the resolution to dissolve is $10 per day. However, there are some special rules, depending on the situation, type of business and the type of liquidation. A corporation, or farmer’s cooperative, must file form 966 if it plans to dissolve the corporation or liquidate.

That Section, However, Has No Provision For Penalties For Violations Of 6043(A).

Get information on coronavirus relief for businesses. For purposes of determining gain or loss, the However, the maximum penalty for the organization for failing to file any single form 966 is $5,000. This is especially true when there are foreign corporations involved, which may lead to form 5471 penalties and an.

Distribution Of Property Corporation Must Recognize Gain Or Loss On The Distribution Of Its Assets In The Complete Liquidation Of Its Stock.

However, there are some special rules, depending on the situation, type of business and the type of liquidation. A corporation, or farmer’s cooperative, must file form 966 if it plans to dissolve the corporation or liquidate the company’s stock, in accordance with internal revenue code section 6043(a). Web penalties for failing to file documents required by section 6043 of the tax code are spelled out in section 6652. Web form 966 penalty vs indirect penalty.

Web The Basic Penalty For Failing To File A Form 966 Within 30 Days Of Adopting The Resolution To Dissolve Is $10 Per Day.

Web who must file form 966? Web they must file form 966, corporate dissolution or liquidation, if they adopt a resolution or plan to dissolve the corporation or liquidate any of its stock. Web once a corporation adopts a plan of liquidation and files the proper state paperwork (if required), it must send form 966, corporate dissolution or liquidation, with a copy of the plan to the irs within 30 days after the date of the adoption. Absent a penalty authorized in the law, there is literally no penalty for failing to file form 966.

A Corporation (Or A Farmer’s Cooperative) Files This Form If It Adopts A Resolution Or Plan To Dissolve The Corporation Or Liquidate Any Of Its Stock.

6043(a) requires a corporation to file a form 966 within 30 days of adopting a plan of liquidation or dissolution, there does not appear to be any specific penalty attached for failing to file it. Closing your business can be a difficult and challenging task. Web information about form 966, corporate dissolution or liquidation, including recent updates, related forms and instructions on how to file. Web where to file file form 966 with the internal revenue service center at the address where the corporation (or cooperative) files its income tax return.